November property market update (2023)

- Posted By Nikki Montaser

National residential rental vacancy rates continue to fall, with October experiencing a 1.0% vacancy, tightening the rental crisis across most capital cities and regional areas. Over the past 30 days, national rental values increased by a combined 1.6%, while combined capital city and national sales asking prices remained steady.

Vacancy rates

National residential rental vacancy rates continue to fall, with October experiencing a 1.0% vacancy, following a similar trend to September, the tightening was experienced across both capital city and regional areas.

Available rental dwellings were reduced by 2,353 dwellings, resulting in 30,307 total vacancies. Significant pressure was experienced in Brisbane, Perth and Adelaide, with vacancy rates of 0.9%, 0.4% and 0.4% respectively.

Louis Christopher, Managing Director of SQM Research said, “After a minor reprieve earlier this year, we are back to the record low in rental vacancies of 1.0%. Vacancies have been tightening again across the nation. They are tightening in our regions as well as our cities.”

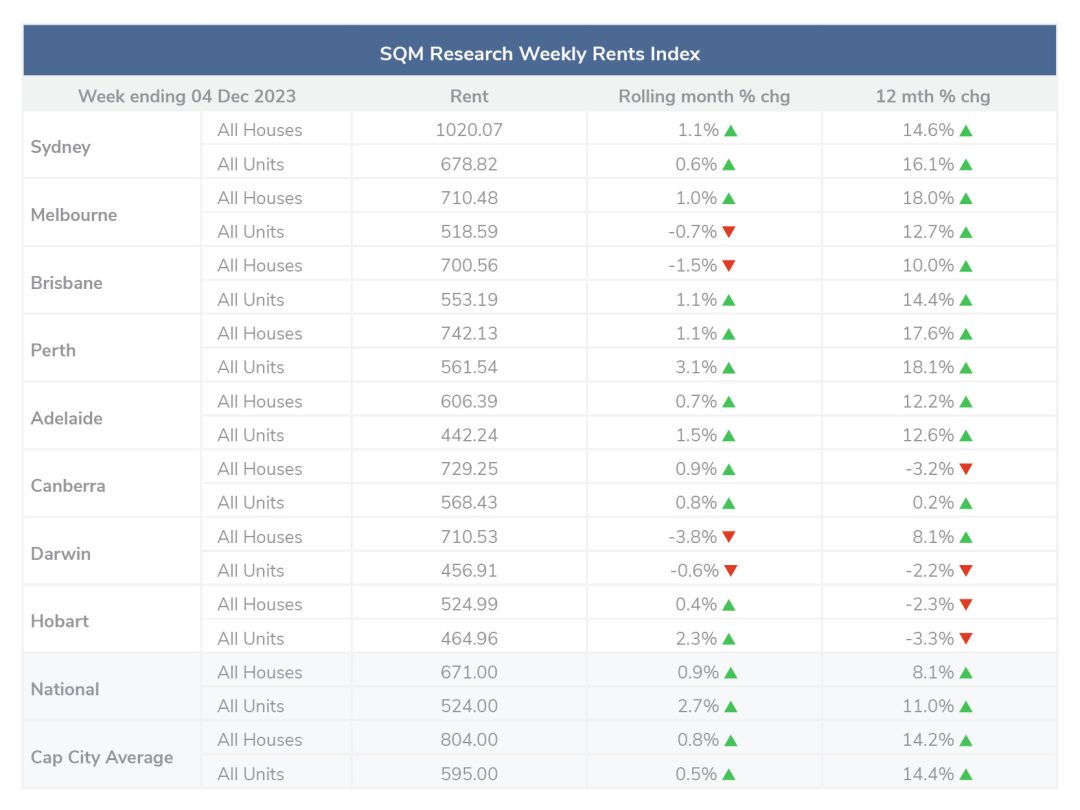

Rental values

Over the past 30 days to 4 December 2023, national weekly asking prices rose by 0.9% for houses and 2.7% for units. The capital city average weekly rent increased by 0.8% for houses and 0.5% for units

Compared to last year, the national asking prices increased by 8.1% for houses and 11% for units. The capital city average asking price increased by 14.2% for houses and 14.4% for units.

On 4 December 2023, the national median weekly asking rent was $671 per week for a house and $524 per week for a unit. The median capital city asking rent for a house was $804 per week for a house and $595 per week for a unit.

Louis Christopher, Managing Director of SQM Research said, “The prospect of an easing in rents over the next six months is very unlikely to occur. And most likely, market rental increases will continue to rise between 10 to 15%. Such rises will continue to work against the RBA’s objective of bringing back inflation to 2% to 3%.

Given 2024 is very likely to see a fall in dwelling completion to about 153,000 dwellings, the only real prospect of having some relief in the rental market next year is a cap on migration rates. I have no doubt the runaway population growth Australia has had since the start of 2022 is directly contributing to our rental crisis and towards other price rises in the greater economy.”

Property prices

National total property listings increased by 1.6% in November, with large increases seen in Canberra and Hobart, while Sydney remained surprisingly steady across a typically busy selling month. Darwin eas the only capital city to experience a decrease in total listings.

Over the past 30 days to 5 December 2023, national combined dwelling asking prices have remained steady, with a slight increase of 0.6% for houses to $884,667 and 0.7% for units to $523,043. Capital city average asking prices have increased 1.2% for houses to $1,321,456 and a marginal 0.8% increase for units to $656,320.

Compared to this time last year, national asking prices have increased 7.2% for houses and 3.7% for units, while capital city averages increased 9.9% for houses and 5.4% for units.

Louis Christopher, Managing Director of SQM Research said, “The spring selling season has been overall, robust for listings. However, I was a little surprised we did not record a surge in November listing counts, which came in at very similar levels to the month of October.

Going forward, we expect the market to enter its year-end hiatus from about the 18th of December. We anticipate a quiet summer holiday period for listings, notwithstanding the normal surges in property activity in our coastal holiday locations.”

Cash rate and predictions

November saw the RBA hold the cash rate target by +25 basis points to 4.35%

Michele Bullock, Governor: Monetary Policy Decision commented, “Inflation in Australia has passed its peak but is still too high and is proving more persistent than expected a few months ago. The latest reading on CPI inflation indicates that while goods price inflation has eased further, the prices of many services are continuing to rise briskly. While the central forecast is for CPI inflation to continue to decline, progress looks to be slower than earlier expected. CPI inflation is now expected to be around 3½ per cent by the end of 2024 and at the top of the target range of 2 to 3 percent by the end of 2025.”

Disclaimer: The information enclosed has been sourced from SQM Research and Reserve Bank of Australia, and is provided for general information only. It should not be taken as constituting professional advice.

PropertyMe is not a financial adviser. You should consider seeking independent legal, financial, taxation, or other advice to check how the information relates to your unique circumstances.

We link to external sites for your convenience. We are selective about which external sites we link to, but we do not endorse external sites. When following links to other websites, we encourage you to examine the copyright, privacy, and disclaimer notices on those websites.

Article posted by Property Me.